Starch Industry EU Market Report

Published March 04, 2025

As we move into 2025, the European market for starch and starch derivatives is navigating a complex landscape marked by significant cost pressures, fluctuating raw material prices, and an evolving economic environment. This article provides a comprehensive update on the current state of the market, focusing on the key factors affecting processors, the broader macroeconomic outlook, and the dynamics within the starch and starch derivatives sector. By examining these elements, we aim to offer valuable insights into the challenges and opportunities that lie ahead for industry stakeholders.

Rising Costs for Starch Processors: A Comprehensive Look

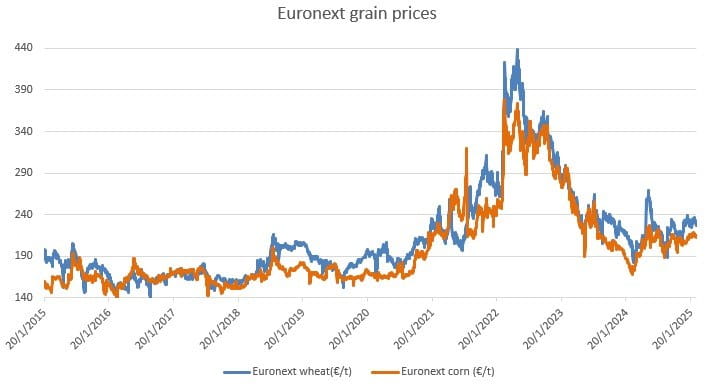

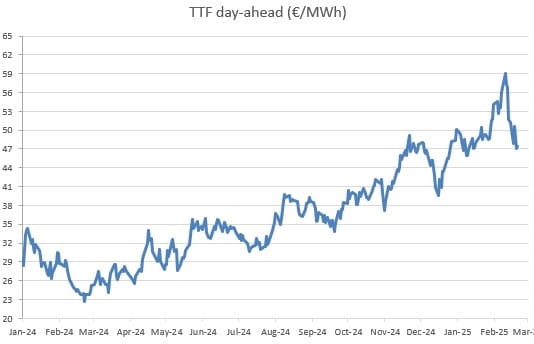

Starch processors in the EU are facing significant cost pressures due to various factors. The prices of raw materials, particularly grains, have been rising since the lows traded end of August 2024 and remain volatile. For example, the March 2025 futures for Euronext wheat and corn have seen significant increases, reflecting tighter supply and demand balances following a disappointing harvest. Geopolitics (war in Ukraine and new administration in the US) are bringing uncertainty hence volatility. Quality concerns also persist, with non-GMO, good quality corn being scarce in the EU. Additionally, European gas prices surged to a two-year high above €57/MWh on 11 February due to cooler temperatures and concerns about storage refilling needs, representing a 65% increase from mid-September levels. Despite the recent drop in prices driven by peace talks on Ukraine and the prospect of relaxing EU storage targets, the current price level still remains three times above historical average (before war) and any small changes in the gas fundamentals can generate large swings in prices. The freight market continues to be challenging, with high costs driven by a structural lack of truck drivers—expected to reach a shortage of 1 million drivers by 2030—environmental surcharges and rising maintenance costs. The costs of chemicals and packaging continue to be high, with the prices of paper bags going up due to supply and demand imbalances, and the cost of hydrogen rising in line with energy trends

Economic Outlook: Positive Signs Accompanied by Challenges

The global economic environment is showing signs of improvement, with steady Gross Domestic Product (GDP) growth and overall eroding inflation expected in 2025. The IMF forecasts a global real GDP growth of 3.3% for the year, up from 3.2% in 2024. This growth is supported by strong labor markets, easing inflation, and recovering supply conditions. In the EU, GDP growth is expected to be slightly positive at 1.1% for 2025, with inflation stabilizing around 2.1%. The European Central Bank (ECB) is anticipated to make two further rate cuts, which could introduce some volatility in grain and energy prices. The food industry, a major outlet for starch processors, is showing recovery signs with a 1% volume increase in Europe and a 1.5% rise in the US for 2024. This trend is expected to continue into 2025. The paper and board industry is also expected to recover progressively, driven by an enhanced economic environment, with EU paper and board production remaining 5% higher than in 2023 according to the Confederation of European Paper Industries (CEPI).

Dynamics of the Starch and Starch Derivatives Market

The global market for starch and starch derivatives is improving, supported by better economic conditions. Historically, the demand for starch and derivatives has been growing at an average rate above 2% year-on-year. However, the COVID-19 pandemic negatively impacted demand. After a recovery in 2021, the economic slowdown again lowered the growth rate of starch derivatives demand. In 2024, we believe that market demand for starch derivatives grew by 7% compared to the previous year, and a gradual recovery is expected to continue in 2025. In the EU, both food and industrial-grade starches are seeing growing demand. The usage of industrial starch was up in both graphic paper and packaging paper production over 2024. The food industry is driving the usage of starch sweeteners, with an 8% increase in starch sweeteners’ usage in 2024 compared to the previous year.

Conclusion

Starch derivative processors continue to face significant cost pressures, with rising and volatile grain market prices, persistent quality issues, and surging energy costs. The freight market remains challenging, and other costs, including chemicals, packaging, labor, and maintenance, continue to exert pressure on processors. Despite these challenges, the economic environment is improving, with steady GDP growth and easing inflation positively impacting businesses and households. The food industry, which is the main outlet for starch processors, is showing formal recovery signs and is expected to continue improving as inflation eases. The paper and board industry, which is the second main outlet for starch processors, is expected to pursue a progressive recovery as the economic environment improves. The global market for starch and starch derivatives is improving, with market demand expected to continue growing over 2025. Starch derivative processors must find the right balance in their processes to cover high costs and remain competitive.

In this dynamic environment, Roquette remains committed to providing high-quality products and solutions to meet the evolving needs of the market. ting this complex landscape.